Here we are providing CBSE Previous Year Question Papers Class 6 to 12 solved with soutions CBSE Class 12 Previous Year Question Papers With Solutions pdf Accountancy Accountancy sample paper class 12, Accountancy previous year question paper class 12, cbse class 12 Accountancy sample paper, cbse class 12 Accountancy sample paper 2020, Accountancy sample paper class 12 2020, cbse sample paper 2020 class 12 Account Practice of previous year question papers and sample papers protects each and every student to score bad marks in exams.If any student of CBSE Board continuously practices last year question paper student will easily score high marks in tests. Fortunately earlier year question papers can assist the understudies with scoring great in the tests. Unraveling previous year question paper class 12 Accountancy is significant for understudies who will show up for Class 12 Board tests.

(Accounting for Not-for-Profit Organizations, Partnership Firms and Companies)

Question 1: (Marks 1)

Srishti, Nitya and Anand were partners in a firm sharing profits and losses in the ratio of 3 : 2 : 1. Srishti retired from the firm selling her share of profits to Nitya and Anand in the ratio of 2 : 1. The new profit sharing ratio between Nitya and Anand will be :

(A) 3 : 2

(B) 17 : 11

(C) 2 : 1

(D) 19 : 11

Answer :

(C)/ 2:1

Question 2: (Marks 1)

Which of the following is not a revenue receipt ?

(A) Donations for Tournament

(B) Government Grants

(C) Subscriptions

(D) Entrance Fees

Answer :

(A)/ Donations for Tournament

Question 3: (Marks 1)

Nominal share capital is :

(A) That part of authorised capital which is issued by the company.

(B) The amount of capital which is actually applied by prospective shareholders.

(C) The amount of capital which is paid by the shareholders.

(D) The maximum amount of share capital that a company is authorised to issue.

Answer :

(D)/ The maximum amount of share capital that a company is authorized to issue.

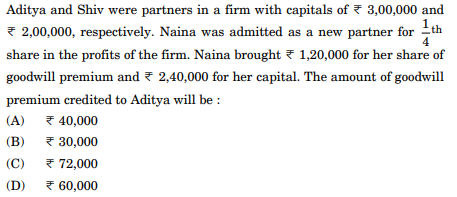

Question 4: (Marks 1)

Answer :

(D)/ ₹60,000

Question 5: (Marks 1)

Distinguish between Income and Expenditure Account and Receipts and Payments Account on the basis of ‘Nature of items’.

Answer :

Income and Expenditure Account records items of revenue nature while Receipts and Payments Account records items of both capital and revenue nature.

Question 6: (Marks 1)

Vidit and Seema were partners in a firm sharing profits and losses in the ratio of 3 : 2. Their capitals were ₹ 1,20,000 and ₹ 2,40,000, respectively. They were entitled to interest on capitals @ 10% p.a. The firm earned a profit of ₹ 18,000 during the year. The interest on Vidit’s capital will be :

(A) ₹ 12,000

(B) ₹ 10,800

(C) ₹ 7,200

(D) ₹ 6,000

Answer :

(D)/ ₹6,000

Question 7: (Marks 1)

At the time of admission of a new partner in the firm, the new partner compensates the old partners for their loss of share in the super-profits of the firm for which he brings in an additional amount which is known as ___________ .

Answer :

Premium for goodwill/ Premium/ Goodwill

Question 8: (Marks 1)

Pragya Ltd. forfeited 8,000 equity shares of ₹ 100 each issued at a premium of 10% for non-payment of first and final call of ₹ 30 per share. The maximum amount of discount at which these shares can be reissued will be :

(A) ₹ 80,000

(B) ₹ 3,20,000

(C) ₹5,60,000

(D) ₹ 2,40,000

Answer :

(C)/ ₹5,60,000

Question 9: (Marks 1)

What is meant by ‘Issue of Debentures as a Collateral Security’ ?

Answer :

Issue of debentures as a collateral security means debentures issued as secondary security when the company obtains a loan.

Question 10: (Marks 1)

Utsav Ltd. decided to redeem its 4,000, 9% Debentures of ₹ 100 each which were issued at a discount of 8%, and were redeemable at a premium of 10%. The amount transferred to Debenture Redemption Reserve will be :

(A) ₹ 4,00,000

(B) ₹ 2,00,000

(C) ₹ 1,10,000

(D) ₹ 1,00,000

Answer :

(D)/ 1,00,000

Question 11: (Marks 1)

‘Interest paid on debentures is a charge against the profits of the company.’ Is this statement correct ? Give reason in support of your answer.

Answer :

Yes.

Reason: Interest on debentures has to be paid whether the company earns profit or not.

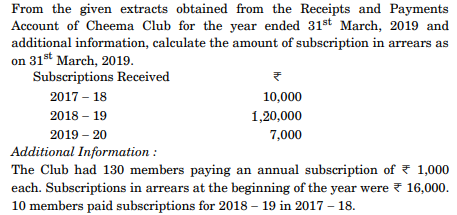

Question 12: (Marks 1)

Answer :

₹6,000

Question 13: (Marks 1)

The directors of Axim Ltd. forfeited 20,000 equity shares of ₹ 10 each, ₹ 8 per share called up for non-payment of first call of ₹ 2 per share. Final call of ₹ 2 per share has not been yet called. Half of the forfeited shares were reissued as fully paid up for ₹ 15 per share. The amount transferred to Capital Reserve will be :

(A) ₹ 2,00,000

(B) ₹ 1,20,000

(C) ₹ 60,000

(D) ₹ 40,000

Answer :

(C)/ ₹60,000

Question 14: (Marks 3)

Answer :

given.

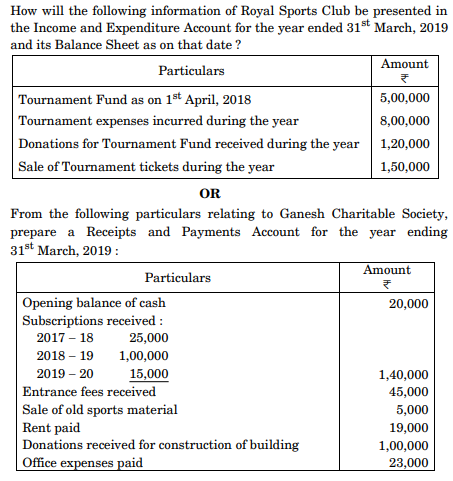

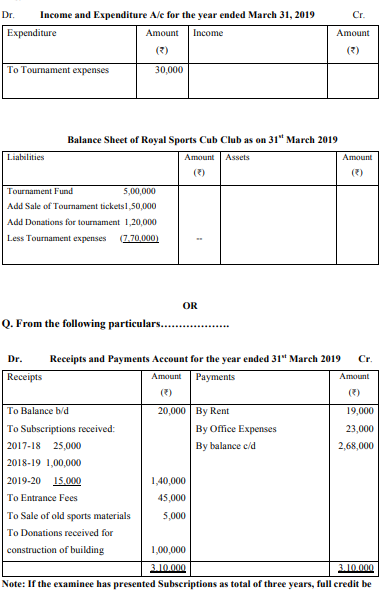

Question 15: (Marks 4)

Answer :

Question 16: (Marks 4)

Answer :

Question 17: (Marks 4)

Answer :

Question 18: (Marks 1)

Answer :

Question 19: (Marks 6)

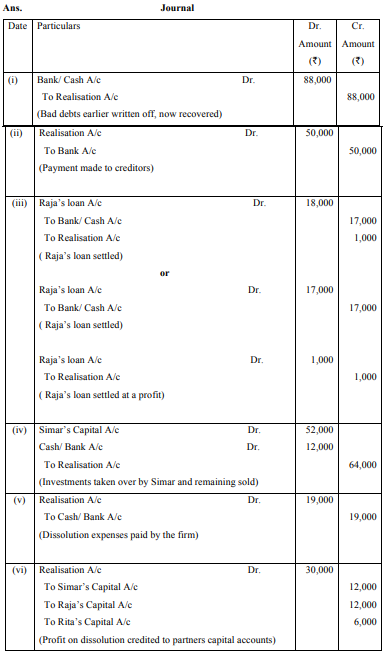

Simar, Raja and Rita were partners in a firm sharing profits and losses in the ratio of 2 : 2 : 1. The firm was dissolved on 31st March, 2019. After the transfer of assets (other than cash) and external liabilities to the Realization Account, the following transactions took place :

(i) A debtor whose debt of ₹ 90,000 had been written off as bad, paid ₹ 88,000 in full settlement.

(ii) Creditors to whom ₹ 1,21,000 were due to be paid, accepted stock at ₹ 71,000 and the balance was paid to them by a cheque.

(iii) Raja had given a loan to the firm of ₹ 18,000. He was paid ₹ 17,000 in full settlement of his loan.

(iv) Investments were ₹ 53,000 out of which investments worth ₹ 43,000 were taken over by Simar at ₹ 52,000 and the balance of the investments were sold for ₹ 12,000.

(v) Expenses on dissolution amounted to ₹ 19,000 and the same were paid by the firm.

(vi) Profit on dissolution amounted to ₹ 30,000. Pass the necessary journal entries for the above transactions in the books of the firm.

Answer :

Question 20: (Marks 6)

(i) Kati Ltd. issued 8,000, 9% debentures of ₹ 100 each at a discount of 10%. The full amount was payable on application. Applications were received for 9,000 debentures and allotment was made on pro-rata basis.

Pass the necessary journal entries for the above transactions in the books of Kati Ltd.

(ii) Pivot Ltd. issued 40,000, 11% debentures of ₹ 100 each on 1st April, 2015. Half of the debentures were due for redemption on 31st March, 2019. The company decided to transfer the minimum required amount to Debenture Redemption Reserve on 31st March, 2018 and invested the necessary amount in Debenture Redemption Investments on 30th April, 2018. Pass the necessary journal entries for Redemption of Debentures.

OR

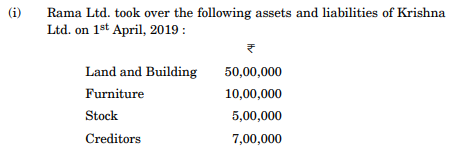

The purchase consideration of ₹ 60,00,000 was paid by issuing 12% debentures of ₹ 100 each at a premium of 20%.

Pass the necessary journal entries for the above in the books of Rama Ltd.

(ii) On 1st April, 2018, Sakshi Ltd. issued 1,000, 11% Debentures of ₹ 100 each at a discount of 6%, redeemable at a premium of 5% after three years.

Pass the necessary journal entries for the issue of debentures in the books of Sakshi Ltd.

(iii) On 1st April, 2016, Canara Bank issued 5,000, 9% debentures of ₹ 100 each at a premium of 6%, redeemable on 31st March, 2019, at a premium of 10%. The issue was fully subscribed.

Pass the necessary journal entries for redemption of debentures in the books of Canara Bank.

Answer :

Question 21: (Marks 8)

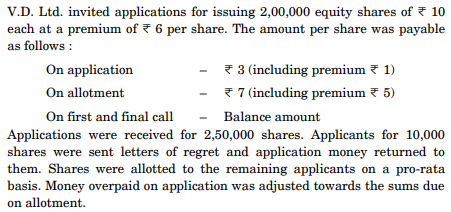

The company received all the money due on allotment except from Agam, who was allotted 1,000 shares. Her shares were forfeited immediately after allotment. Afterwards, the first and final call was made. Seema, the holder of 2,000 shares, did not pay the first and final call on her shares. Her shares were also forfeited. 50% of the forfeited shares, each of Agam and Seema, were reissued as fully paid-up @ ₹ 16 per share. Pass the necessary journal entries to record the above transactions in the books of V.D. Ltd.

OR

Konark Ltd. invited applications for issuing 3,00,000 shares of ₹ 10 each. The amount per share was payable as follows : ₹ 3 on application, ₹ 3 on allotment, and ₹ 4 on first and final call. The company received applications for 4,00,000 shares. Allotment was done as follows :

(i) Applicants of 2,40,000 shares were allotted 2,00,000 shares.

(ii) Applicants of 1,20,000 shares were allotted 80,000 shares.

(iii) Remaining applicants were allotted 20,000 shares.

Money overpaid on applications was adjusted towards sums due on allotment. Divij, a shareholder, belonging to group (ii), who had applied for 6,000 shares, failed to pay allotment and call money. Faisal, another shareholder, who was allotted 10,000 shares, paid the call money along with allotment. Faisal belonged to group (i).

Divij’s shares were forfeited after the first and final call. Half of the forfeited shares were reissued @ ₹ 10 per share fully paid. Pass the necessary journal entries to record the above transactions in the books of the company.

Answer :

Question 22: (Marks 8)

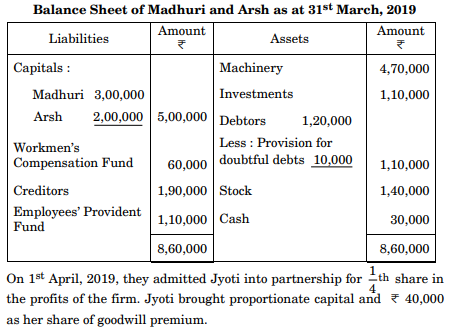

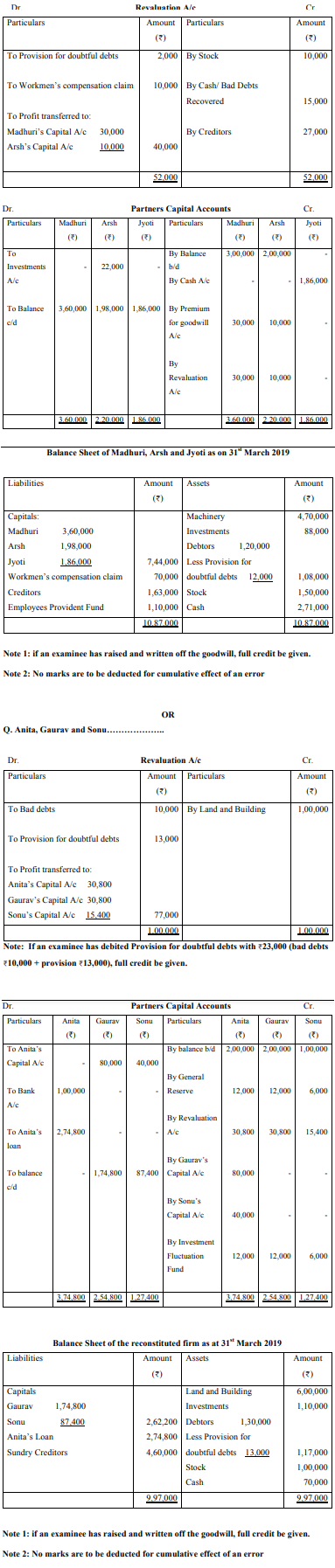

Madhuri and Arsh were partners in a firm sharing profits and losses in the ratio of 3 : 1. Their Balance Sheet as at 31st March, 2019, was as follows :

The following terms were agreed upon :

(i) Provision for doubtful debts was to be maintained at 10% on debtors.

(ii) Stock was undervalued by ₹ 10,000.

(iii) An old customer whose account was written off as bad, paid ₹ 15,000.

(iv) 20% of the investments were taken over by Arsh at book value.

(v) Claim on account of workmen’s compensation amounted to ₹ 70,000.

(vi) Creditors included a sum of ₹ 27,000 which was not likely to be claimed.

Prepare Revaluation Account, Partners’ Capital Accounts, and the Balance Sheet of the reconstituted firm.

OR

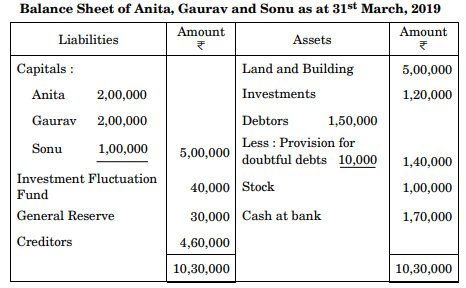

Anita, Gaurav and Sonu were partners in a firm sharing profits and losses in proportion to their capitals. Their Balance Sheet as at 31st March, 2019 was as follows :

On the above date, Anita retired from the firm and the remaining partners decided to carry on the business. It was agreed to revalue the assets and reassess the liabilities as follows :

(i) Goodwill of the firm was valued at ₹ 3,00,000 and Anita’s share of goodwill was adjusted in the capital accounts of the remaining partners, Gaurav and Sonu.

(ii) Land and Building was to be brought up to 120% of its book value.

(iii) Bad debts amounted to ₹ 20,000. A provision for doubtful debts was to be maintained at 10% on debtors.

(iv) Market value of investments was ₹ 1,10,000.

(v) ₹ 1,00,000 was paid immediately by cheque to Anita out of the amount due and the balance was to be transferred to her loan account which was to be paid in two equal annual instalments along with interest @ 10% p.a.

Prepare the Revaluation Account, Partners’ Capital Accounts and the Balance Sheet of the reconstituted firm on Anita’s retirement.

Answer :

OPTION 1

(Analysis of Financial Statements)

Question 23: (Marks 1)

An investment normally qualifies as a cash equivalent only when it has a maturity of _________ months or less from the date of acquisition.

Answer :

Three

Question 24: (Marks 1)

X Ltd. purchased furniture for ₹ 20,00,000 paying 60% by issue of equity shares of ₹ 10 each and the balance by a cheque. This transaction will result in :

(A) Cash used in investing activities ₹ 20,00,000.

(B) Cash generated from financing activities ₹ 12,00,000.

(C) Increase in cash and cash equivalents ₹ 8,00,000.

(D) Cash used in investing activities ₹ 8,00,000.

Answer :

(D). Cash used in investing activities ₹8,00,000

Question 25: (Marks 1)

Which of the following is not a limitation of ‘Financial Statements Analysis’ ?

(A) It is affected by personal bias.

(B) Inter-firm comparative study possible.

(C) Lack of qualitative analysis.

(D) Ignores price level changes.

Answer :

(B)/ Inter firm comparative study possible

Question 26: (Marks 1)

State the objective of preparing ‘Cash Flow Statement’.

Answer :

The objective of preparing Cash Flow Statement is to provide useful information about Cash Flows (Inflows & outflow) of an enterprise during a particular period under various heads of activities.

Question 27: (Marks 1)

Under which of the following head/subhead is ‘Forfeited Shares’ presented in the Balance Sheet of a company ?

(A) Reserves and Surplus

(B) Share Capital

(C) Other Long-term Liabilities

(D) Other Current Liabilities

Answer :

(B)/ Share capital

Question 28: (Marks 1)

Which of the following is not a subhead under the Current Assets ?

(A) Cash and Cash Equivalents

(B) Trademarks

(C) Short-term Loans and Advances

(D) Inventories

Answer :

(B)/ Trademarks

Question 29: (Marks 1)

What will be the effect of purchase of goods for cash ₹ 3,000 on Gross Profit Ratio ?

Answer :

No Effect

Question 30: (Marks 3)

From the following information obtained from the books of P. Ltd., calculate, (i) Return on Investment, and (ii) Debt-Equity Ratio : Information :

Net Profit after interest and tax ₹ 6,00,000; 6% Debentures ₹ 10,00,000; Capital employed ₹ 20,00,000, and Tax rate 40%.

OR

(i) Current Liabilities ₹ 1,50,000, Current Assets ₹ 2,80,000, Inventories ₹ 40,000, Advance Tax ₹ 30,000, and Prepaid Rent ₹ 10,000. Calculate Quick Ratio.

(ii) Average Inventory ₹ 60,000, Revenue from Operations ₹ 6,00,000, the rate of Gross Loss on Sales is 10%. Calculate the Inventory Turnover Ratio.

Answer :

Return on Investment = Net profit before interest and tax/ Capital Employed x 100…..1/2

Net profit before interest and tax = Net profit after interest and tax + tax + interest

= ₹6,00,000 + ₹4,00,000 + ₹60,000

= ₹10,60,000……………………………………1/2

Capital Employed = ₹20,00,000

Return on Investment=₹10,60,000/₹20,00,000 x100

=53%......................................................................................1/2

Debt Equity Ratio = Debt/ Equity ………………………………………………………1/2

Equity = Capital Employed – Debt

=₹20,00,000 – ₹10,00,000

=₹10,00,000……………….………………………………..………………………1/2

Debt Equity Ratio = ₹10,00,000/ ₹10,00,000

=1:1…………………….…………………………………………………1/2

OR

(i) Quick Ratio= Quick Assets/ Current Liabilities …………………….………………1/2

Quick assets= Current assets – Inventories – Advance Tax – Prepaid rent

= ₹2,80,000 - ₹40,000 - ₹30,000 – ₹10,000

= ₹2,00,000 …………………….…………………………………………………1/2

Quick Ratio= ₹2,00,000/₹1,50,000

Quick Ratio =1.33:1…………………….…………………………………………………1/2

(ii) Inventory Turnover ratio= Cost of Revenue from operations / Average Inventor…1/2

Cost of Revenue from operations = Revenue from operations + Gross Loss

Gross Loss= 10/100 x ₹6,00,000 = ₹60,000

Cost of Revenue from operations = ₹6,60,000……………………………………………1/2

Average Inventory= ₹60,000

Inventory Turnover ratio = ₹6,60,000/ ₹60,000

=11 times…………………………………………1/2

Question 31: (Marks 4)

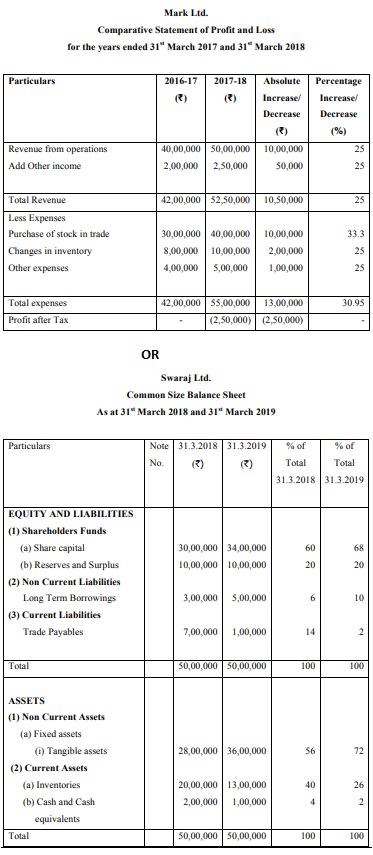

From the following particulars obtained from the books of Mark Ltd., prepare a Comparative Statement of Profit and Loss :

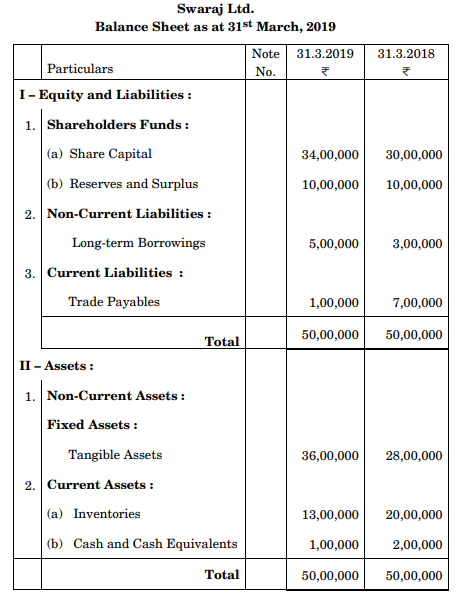

From the following Balance Sheet of Swaraj Ltd., as at 31st March, 2019, prepare a common size Balance Sheet :

Answer :

Question 32: (Marks 6)

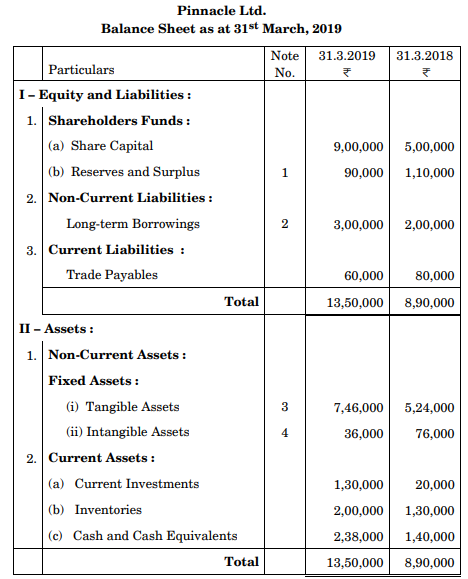

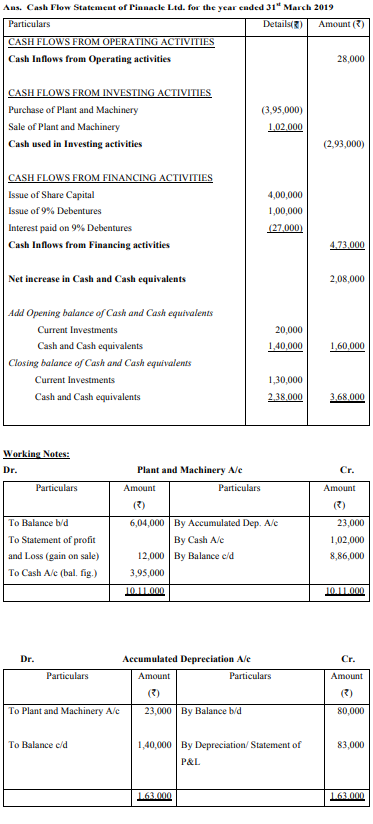

Cash flow from the operating activities of Pinnacle Ltd. for the year ended 31st March, 2019 was ₹ 28,000. The Balance Sheet along with notes to accounts of Pinnacle Ltd. as at 31st March, 2019 is given below :

Answer :

OPTION 2

(Computerised Accounting)

Question 23: (Marks 1)

Hardware refers to :

(A) System software and application software.

(B) Computer associated peripherals and their network.

(C) A logical sequence of actions to perform a task.

(D) All of the above.

Answer :

(b) / Computer associated peripherals their network.

Question 24: (Marks 1)

To safeguard assets and optimise the use of resources, a business :

(A) Keeps internal controls.

(B) Only tries to achieve maximum revenue.

(C) Only ensures accurate accounting records.

(D) Only safeguards assets.

Answer :

(a) / Keeps internal controls.

Question 25: (Marks 1)

The existence of data in a ‘primary key’ field is :

(A) Not necessarily required.

(B) Required but need not be unique.

(C) Required and must be unique.

(D) All of the above.

Answer :

(c) / Required and must be unique.

Question 26: (Marks 1)

A ##### error appears when :

(A) A negative data is used.

(B) Column is not wide enough.

(C) Negative time is used.

(D) All of the above.

Answer :

(d) / All of above.

Question 27: (Marks 1)

The ___________ provides real power to database in terms of its capacities to answer complex requests involving data to be taken from ___________ tables.

Answer :

The Query provides real power to database in terms of its capacities to answer complex requests involving data to be taken from multiple tables.

Question 28: (Marks 1)

A code which consists of alphabet or abbreviation as symbol to codify a piece of information is known as ___________ code.

Answer :

A code which consists of alphabet or abbreviation as symbol to codify a piece of information is known as Mnemonic code.

Question 29: (Marks 1)

A ___________ voucher is used for adjustment of non-cash transaction in the ledger.

Answer :

A Journal voucher is used for adjustment of non cash transactions in the ledger.

Question 30: (Marks 3)

What information is provided by a salary bill ?

OR

List the various attributes of a ‘payroll’ database.

Answer :

The following information is provided by a salary bill:

(i) Maintaining payroll related data such as employee number, Name, Attendance, Basic Pay, applicable Dearness and other allowances and deductions to be made.

(ii) Periodic payroll computations: The payroll computations include the calculation of various earnings and deduction heads which are to be derived from basic values such as (basic salary, number of days under leave without pay and unauthorized absence, etc) as per the formulae.

(iii) Preparation of salary statement and employee salary slip.

(iv) Generation of advice to bank.

OR

(i) Employees personal details

(a) Employee In

(b) Name

(c) Designation

(d) Location

(ii) Employees pay details

(a) Basic pay

(b) DA

(c) HRA

(d) TA

(e) Provident fund

(f) Any deduction for loan etc.

This information helps in calculating Gross and net salary.

Question 31: (Marks 4)

Explain ‘closing entry’ and ‘adjustment entry’ with the help of examples.

OR

Explain any four advantages expected by the user for paying high price for a chosen server database.

Answer :

Closing Entry :

Entries required to make trading account and profit and loss account are known as closing entries.

After the Trial balance is prepared all the expenses are debited to the respective accounts to prepare trading and profit and loss account similarly income or expenditure for the trading period. These are the entries to record outstanding and prepaid.

Adjusting Entry :

Adjusting entries are the figures related to income or expenditure for the trading period. These are the entries to record outstanding and prepaid.

OR

Any Four of the following:

(i) Flexibility

(ii) Choice of front and application

(iii) Powerful performance

(iv) Scalability to handle rapidly expanding number of users.

(v) Ease of handling huge amount of data.

Question 32: (Marks 6)

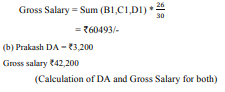

Tolga Ltd. has its offices in Delhi and Chandigarh. HRA for Delhi is ₹ 25,000 and for Chandigarh is ₹ 20,000. DA is calculated on Basic Pay (BP) as 16% for BP ≤ ₹ 22,000 and 12% for BP ≥ ₹ 23,000. Standard number of days are taken as 30 days per month.

Give the formulae and calculate the amount of Gross Salary on Excel for the following employees :

(i) Purnima is working in Delhi office. Her Basic Pay is ₹ 40,000. She has availed four days of leave without pay.

(ii) Prakash is working in Chandigarh office. His Basic Pay is ₹ 20,000. He did not take any leave.

Answer :

Keys

Employee Name = A1

HRA = B1

Basic Pay = C1

DA = D1

Gross Salary = E1

(a) Calculation of DA

D1 = If (C1 ≤ ₹22000, 16%, 12% ) * C1

D1 = If (C1 ≥ ₹23000, 12%, 16% ) * C1

Purnima DA = ₹4,800

Accountancy sample paper class 12, Accountancy previous year question paper class 12, cbse class 12 Accountancy sample paper, cbse class 12 Accountancy sample paper 2020, Accountancy sample paper class 12 2020, cbse sample paper 2020 class 12 Accountancy, class 12 Accountancy sample paper 2020, class 12 important questions Accountancy, cbse class 12 board exam Accountancy paper, Accountancy previous year question papers class 12 with solutions, Accountancy sample paper class 12 2019, cbse class 12 Accountancy question paper 2017 solved pdf, cbse class 12 Accountancy question paper 2018, class 12 Accountancy paper 2019, Accountancy question paper for class 12, cbse class 12 Accountancy paper 2019

Copyright @ ncerthelp.com A free educational website for CBSE, ICSE and UP board.