Here we are providing CBSE Previous Year Question Papers Class 6 to 12 solved with soutions Accountancy Sample Paper for Class 12 With Solution NCERT CBSE Board 2020 Accountancy sample paper class 12, Accountancy previous year question paper class 12, cbse class 12 Accountancy sample paper, cbse class 12 Accountancy sample paper 2020, Accountancy sample paper class 12 2020, cbse sample paper 2020 class 12 Account Practice of previous year question papers and sample papers protects each and every student to score bad marks in exams.If any student of CBSE Board continuously practices last year question paper student will easily score high marks in tests. Fortunately earlier year question papers can assist the understudies with scoring great in the tests. Unraveling previous year question paper class 12 Accountancy is significant for understudies who will show up for Class 12 Board tests.

(Accounting for Not-for-Profit Organizations,

Partnership Firms and Companies)

Question 1: (Marks)

When a company plans to redeem its debentures out of profits, it should transfer minimum ______ % of the face value of the outstanding debentures to Debenture Redemption Reserve out of surplus available for payment of dividend.

Answer :

25

Question 2: (Marks 1)

_______ capital accounts always show a credit balance.

Answer :

Fixed Capital accounts always show a credit balance.

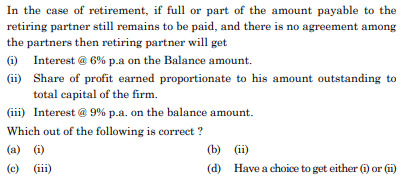

Question 3: (Marks 1)

Answer :

(d)/ Have a choice to get either (i) or (ii)

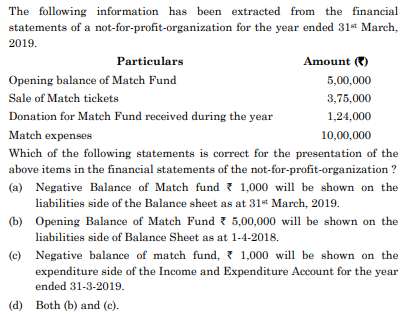

Question 4: (Marks 1)

Answer :

(d)/ Both (b) and (c)

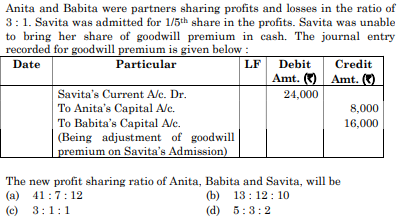

Question 5: (Marks 1)

Answer :

(a)/ 41:7:12

Question 6: (Marks 1)

Amla, Bimla and Kavita were partners sharing profits and losses in the ratio of 4 : 3 : 1. Bimla retires and gives her share of profit to Amla for ₹ 3,600 and to Kavita for ₹ 3,000. The gaining ratio of Amla and Kavita will be :

(a) 4 : 5

(b) 2 : 1

(c) 6 : 5

(d) 4 : 1

Answer :

(c)/ 6:5

Question 7: (Marks 1)

Capital Reserve is created out of ______ profits.

Answer :

Capital Reserve is created out of capital profits

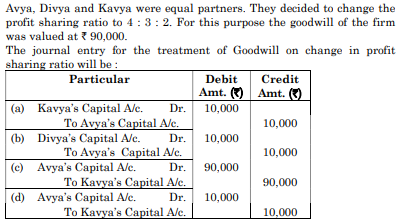

Question 8: (Marks 1)

Answer :

(d)/

Avya’s Capital A/c 10,000 To

Kavya’s capital A/c 10,000

Question 9: (Marks 1)

Mohit, Shobhit and Rohit are partners sharing profits and losses in the ratio 2 : 1 : 1. Rohit is guaranteed a profit of ₹ 14,000. The firm incurred a profit of ₹ 20,000 during the year. Calculate the amount of deficiency borne by Mohit and Shobhit.

Answer :

Mohit ₹6,000 and Shobhit ₹3,000.

Question 10: (Marks 1)

Which of the following is not a purpose for which the Securities Premium amount can be used ?

(a) Issuing fully paid bonus shares to shareholders.

(b) Issuing partly paid up bonus shares to shareholders.

(c) Writing off preliminary expenses of the company.

(d) In purchasing its own shares (buy back)

Answer :

(b)/ Issuing partly paid up bonus shares to shareholders

Question 11: (Marks 1)

Tangible Assets of the firm are ₹ 14,00,000 and outside liabilities are ₹ 4,00,000. Profit of the firm is ₹ 1,50,000 and normal rate of return is 10%. The amount of Capital employed will be

(a) ₹ 10,00,000

(b) ₹ 1,00,000

(c) ₹ 50,000

(d) ₹ 20,000

Answer :

(a)/ ₹10,00,000

Question 12: (Marks 1)

Income and Expenditure Account records :

(a) Receipts and Payments of Revenue and Capital nature both.

(b) Income and Expenditure of Revenue nature only.

(c) Expenditure of Capital nature only.

(d) Receipts of Revenue nature only.

Answer :

(b)/ Income and Expenditure of Revenue nature only.

Question 13: (Marks 1)

When the business of the firm becomes illegal, the way of dissolution of the firm is ________.

Answer :

Compulsory dissolution

Question 14: (Marks 3)

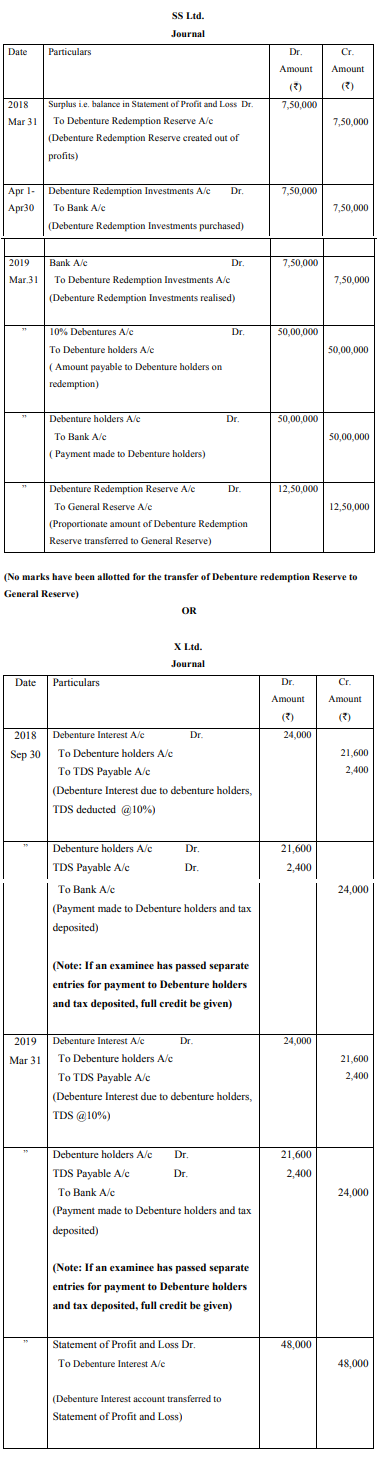

On 31st March 2018 SS Ltd. had 50,000 10% debentures of ₹ 100 each outstanding . These debentures were due for redemption on 31st March, 2019. Debenture Redemption Reserve has a balance of ₹ 5,00,000 on 31st March, 2018. Ignoring the entries for interest, pass the necessary journal entries for redemption of debentures.

OR

X Ltd. has 4,000 12% debentures of ₹ 100 each on 1st April, 2018. According to the terms of issue interest on debentures is payable half yearly on 30th September and 31st March and the rate of tax deducted at source is 10%. Pass necessary journal entries for interest on debentures for the year 2018-19.

Answer :

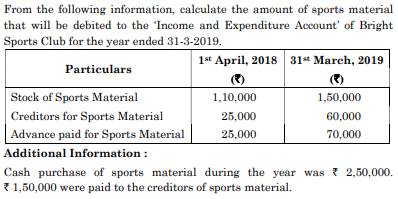

Question 15: (Marks 4)

Answer :

Alternatively:

Credit Purchases= Payment made to creditors+ closing Creditors – Opening Creditors – Closing advance + Opening advance

= ₹1,50,000 + ₹60,000 – ₹25,000 - ₹70,000 + ₹25,000

= ₹1,40,000………………………………………………………2 marks

Sports Materials consumed = Opening stock of Sports Materials + Purchases – Closing Stock of Sports Materials

= ₹1,10,000 + (₹2,50,000 + ₹1,40,000) – ₹1,50,000

= ₹3,50,000…………………………2 marks

Question 16: (Marks 4)

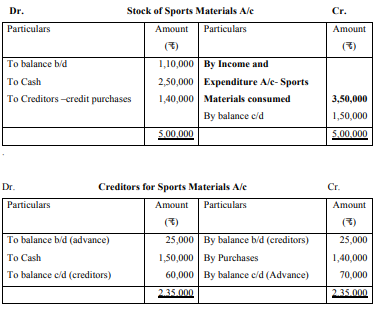

A and B are partners sharing profits and losses in the ratio of 3 : 2. Their capital on 31st March, 2018 after all adjustments stood at ₹ 1,65,500 and ₹ 1,27,600 respectively.

Profits amounting to ₹ 50,000 for the year 2017-18 were distributed after allowing interest on drawings @ 12% p.a. During the year A withdrew ₹ 15,000 at the beginning of every quarter and B withdrew ₹ 40,000 during the year. Partnership deed is silent on interest on drawings but provides for interest on Capital @ 5% p.a. Interest on Capital has not been provided.

Showing your workings clearly, pass the necessary adjustment entry to rectify the above errors.

OR

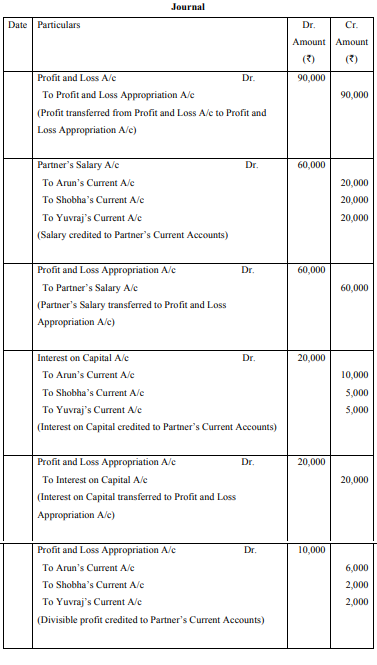

Arun, Shobha and Yuvraj were partners in a firm. On 1st April, 2018 their Fixed Capitals Stood at ₹ 1,00,000, ₹ 50,000 and ₹ 50,000 respectively.

As per the provisions of partnership deed,

(i) Partners were entitled to an annual salary of ₹ 20,000 each.

(ii) Interest on Capital @ 10% p.a. was to be provided.

(iii) Profits were to be shared in the ratio 3 : 1 : 1. Net profit for the year ended 31st March, 2019 was ₹ 90,000.

Pass Journal Entries for the above in the books of the firm.

Answer :

Interest on Drawings:

A: 12/100 x ₹60,000 x 7.5/12 = ₹4,500

B: 12/100 x ₹40,000 x 6/12 = ₹2,400

OR

Question 17: (Marks 4)

Answer :

Question 18: (Marks 4)

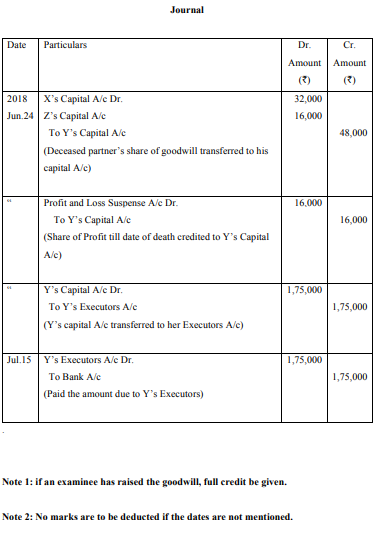

X, Y and Z were partners in a firm sharing profits and losses in the ratio of 2 : 2 : 1. The firm closes its books on 31st March every year. Y died on 24th June, 2018. On Y’s death goodwill of the firm was valued at ₹ 1,20,000. Y’s share in the profits of the firm till the date of death from the last Balance Sheet was to be calculated on the basis of sales. Sales during the year 2017-18 was ₹ 15,00,000 and profit earned during the year was ₹ 3,00,000. Sales from 1st April, 2018 to 24th June, 2018 were ₹ 2,00,000. The total amount payable to Y’s executors on his death was ₹ 1,75,000. This amount was paid to them on 15-7-2018.

Pass the necessary journal entries for the above transactions in the books of the firm.

Answer :

Question 19: (Marks 6)

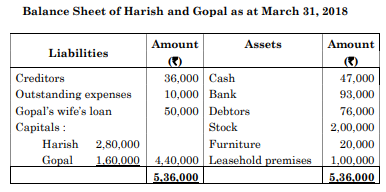

Harish and Gopal were partners in a firm sharing profits in the ratio of 3 : 2. On 31st March, 2018, their Balance Sheet was as follows :

On the above date the firm was dissolved. The various assets were realized and liabilities were settled as under :

(i) Gopal agreed to pay his wife’s loan.

(ii) Leasehold premises realised ₹ 1,50,000 and Debtors ₹ 12,000 less.

(iii) Half of the creditors agreed to accept furniture of the firm as full settlement of their claim and remaining half agreed to accept 10% less.

(iv) 50% stock was taken over by Harish on payment by cheque of ₹ 90,000 and remaining stock was sold for ₹ 94,000.

(v) Realization expenses of ₹ 10,000 were paid by Gopal on behalf of the firm.

Prepare Realization Account.

OR

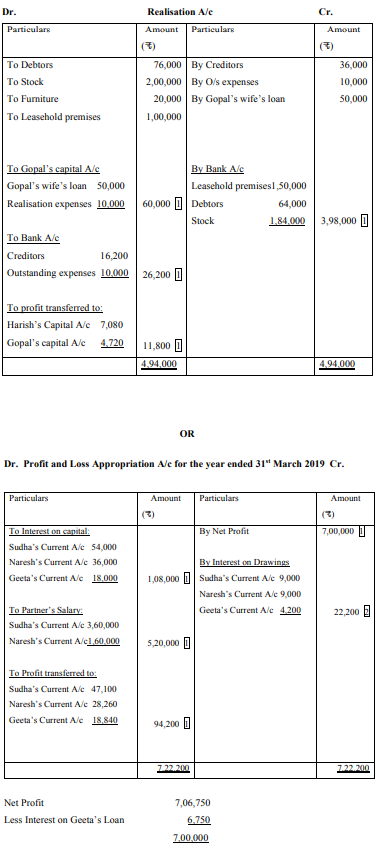

Sudha, Naresh and Geeta were partners in a firm sharing profits in the ratio of 5 : 3 : 2. Their fixed capitals were ₹ 6,00,000; ₹ 4,00,000 and ₹ 2,00,000 respectively. Besides her capital Geeta had given a loan of ₹ 75,000 to the firm. Their partnership deed provided for the following :

(i) Interest on capital @ 9% p.a.

(ii) Interest on partners’ drawings @ 12% p.a.

(iii) Salary to Sudha ₹ 30,000 per month and to Naresh ₹ 40,000 per quarter.

(iv) Interest on Geeta’s loan @ 9% p.a.

During the year Sudha withdrew ₹ 50,000 at the end of each quarter; Naresh withdrew ₹ 50,000 in the beginning of each half year and Geeta withdrew ₹ 70,000 at the end of each half year.

The profit of the firm for the year ended 31-3-2019 before allowing interest on Geeta’s loan was ₹ 7,06,750.

Prepare Profit and Loss Appropriation Account.

Answer :

Question 20: (Marks 6)

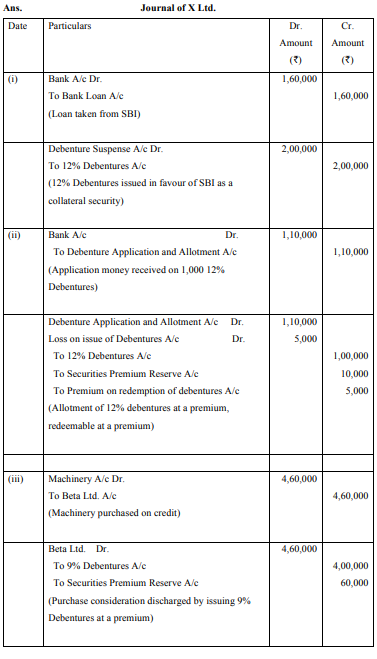

Pass journal entries in the book of X Ltd. in the following cases :

(i) The Company took a loan of ₹ 1,60,000 from SBI and issued 2,000, 12% debentures of ₹ 100 each as collateral security.

(ii) Issued 1,000, 12% debentures of ₹ 100 each at 10% premium, redeemable at a premium of 5%.

(iii) Purchased machinery ₹ 4,60,000, from Beta Ltd. Payment was made by issue of 9% debentures of ₹ 100 each at a premium of 15% redeemable at par.

Answer :

Question 21: (Marks 8)

Zee Ltd. invited applications for issuing 3,40,000 equity shares of ₹ 10 each at a premium of ₹ 5 per share. The amount was payable as follows :

On application ₹ 4 per share (including ₹ 2 premium)

On allotment ₹ 5 per share (including ₹ 2 premium)

On First and Final call – Balance.

Applications for 6,00,000 shares were received. Application for 1,80,000 shares were rejected and application money was refunded. Shares were allotted on prorata basis to the remaining applicants. Excess money received with applications was adjusted towards sum due on allotment. Yamini who had applied for 2100 shares failed to pay allotment money and her shares were forfeited immediately. Vani to whom 6800 shares were allotted paid her entire share money due on allotment. Afterwards First and Final call was made and was duly received. Out of the forfeited shares 850 shares were reissued to Vansh at ₹ 8 per share fully paid up.

Pass necessary journal entries for the above transactions in the books of the company by opening calls-in-arrears and calls-in-advance accounts.

OR

K.N. Ltd. invited applications for issuing 6,00,000 equity shares of ₹ 10 each at a premium of ₹ 3 per share. The amount was payable as follows :

On Application and Allotment ₹ 3 per share.

On First Call ₹ 4 per share.

On Second and Final Call Balance (including premium).

Applications for 8,00,000 shares were received. Applications for 50,000 shares were rejected and the application money was refunded. Shares were allotted to the remaining applicants as follows :

Category I : Those who had applied for 4,00,000 share were allotted 3,00,000 shares on pro-rata basis.

Category II : The remaining applicants were allotted the remaining shares on pro-rata basis.

Excess application money received with applications was adjusted towards sums due on first call. Rakesh to whom 6,000 shares were allotted failed to pay the first call money. Rakesh belonged to category I. His shares were forfeited. The forfeited shares were re-issued at ₹ 13 per share fully paid up. The second call was made afterwards and was duly received.

Pass necessary journal entries for the above transactions in the books of K.N. Ltd.

Answer :

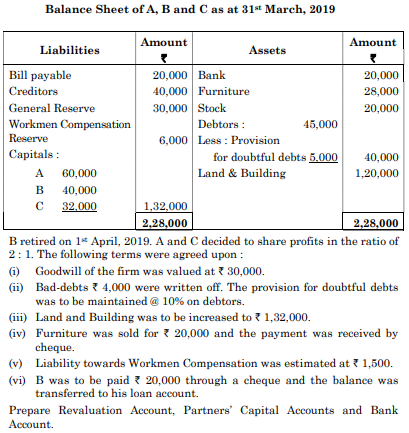

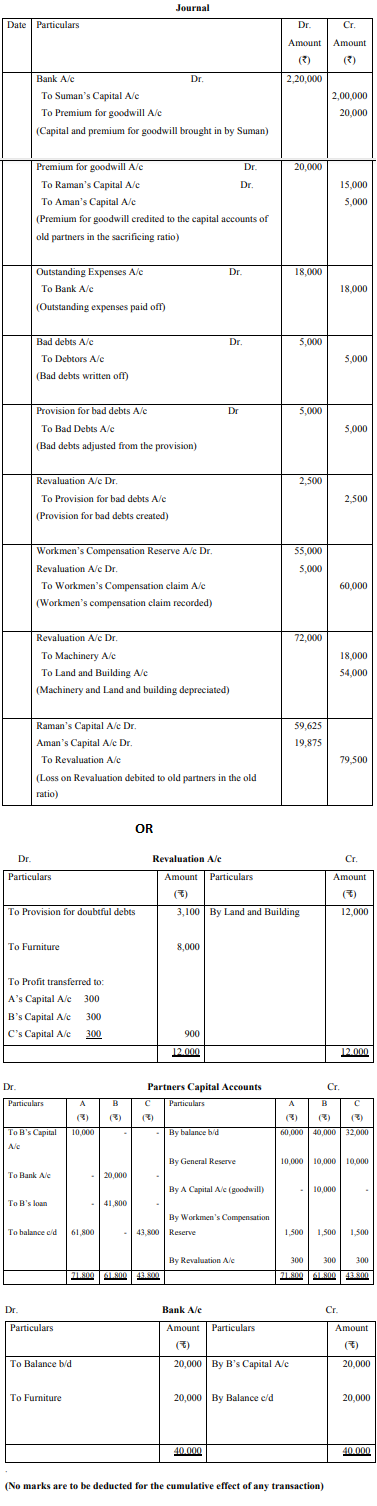

Question 22: (Marks 8)

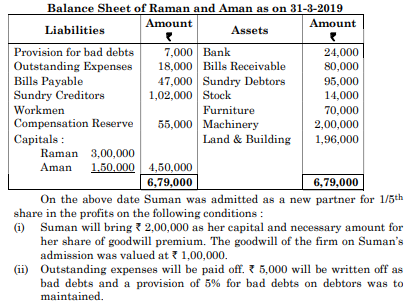

Raman and Aman were partners in a firm and were sharing profits in 3 : 1 ratio. On 31-3-2019 their balance sheet was as follows :

(iii) The liability towards workmen compensation was estimated at ₹ 60,000.

(iv) Machinery was to be depreciated by ₹ 18,000 and Land and Building was to be depreciated by ₹ 54,000. Pass necessary journal entries for the above transactions in the books of the firm.

OR

A, B and C were partners in a firm. Their Balance Sheet as at 31st March, 2019 was as follows :

Answer :

Option – I

(Analysis of Financial Statements)

Question 23: (Marks 1)

The quick ratio of a company is 0.5 : 0.75. Will cash sales of ` 5,000 increase, decrease or not change the ratio ? Give reason in support of your answer.

Answer :

Increase

Reason: Quick assets (cash) with no change in Current Liabilities

Question 24: (Marks 1)

Employee benefit expenses include ___________. (bonus/depreciation/ income tax)

Answer :

Bonus

Question 25: (Marks 1)

Which of the following is not a limitation of analysis of financial statements ?

(a) Window Dressing

(b) Price level changes ignored

(c) Subjectivity

(d) Intra firm comparison possible

Answer :

(d)/ Intra firm comparison possible

Question 26: (Marks 1)

Under which of the following headings/sub-headings, Calls in advance will be presented in the Balance Sheet of a Company as per Schedule III Part I of the Companies Act, 2013 ?

(a) Current Liabilities

(b) Share Capital

(c) Share Application Money Pending Allotment

(d) Reserves and Surplus.

Answer :

(a)/ Current Liabilities

Question 27: (Marks 1)

Interest received in cash from loans and advance is considered as _____ activity while preparing cash flow statement.

Answer :

Investing

Question 28: (Marks 1)

List any two items other than cash in hand and cheques in hand that are presented under the sub-heading ‘Cash and Cash Equivalents’ in the Balance Sheet of a company.

Answer :

Any two of the following :

(i) Balance with banks

(ii) Bank drafts in hand

(iii) Current Investments

(iv) Treasury Bills

(v) Commercial Paper

(vi) Preference Shares redeemable within three months from the date of purchase

(Or any other correct item)

Question 29: (Marks 1)

While preparing cash flow statement, will ‘Cash withdrawn from bank’ result into inflow, outflow or no flow of cash ? Give reason in support of your answer.

Answer :

No Flow

Reason: There is no change in cash and cash equivalents

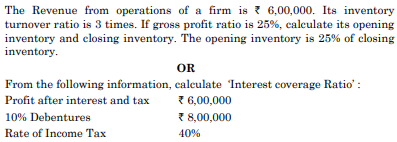

Question 30: (Marks 3)

Answer :

Revenue from Operations= ₹6,00,000

Gross profit = 25/100 x ₹6,00,000 = ₹1,50,000………………………………….…1/2

Cost of Revenue from Operations =₹6,00,000 – ₹1,50,000

= ₹4,50,000……………………………….……1/2

Inventory turnover Ratio = Cost of Revenue from Operations/ Average Inventory… …1/2

ð 3 = ₹4,50,000/ Average Inventory

ð Average Inventory =₹1,50,000…………………….…………………………1/2

Average Inventory = (Opening Inventory + Closing Inventory)/2= ₹1,50,000

ð (1/4 Closing inventory + Closing Inventory)/2 = ₹1,50,000

ð Closing Inventory = ₹2,40,000……………………………………………1/2

ð Opening Inventory = ¼ x ₹2,40,000 = ₹60,000………….………………1/2

OR

Interest Coverage Ratio = Profit before Interest and Tax/ Capital employed x 100…….1

Profit after Interest and Tax = ₹6,00,000

Profit before Interest and Tax = ₹6,00,000 + ₹80,000+₹ 4,00,000………………………1

Interest Coverage Ratio = ₹10,80,000/ ₹80,000

= 13.5 times……………………………………………..………1

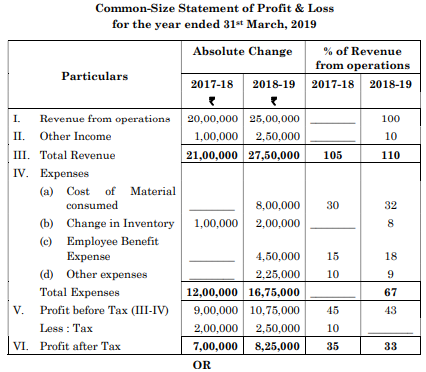

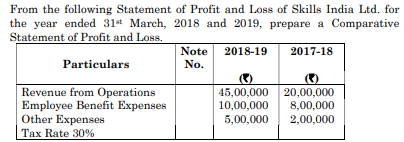

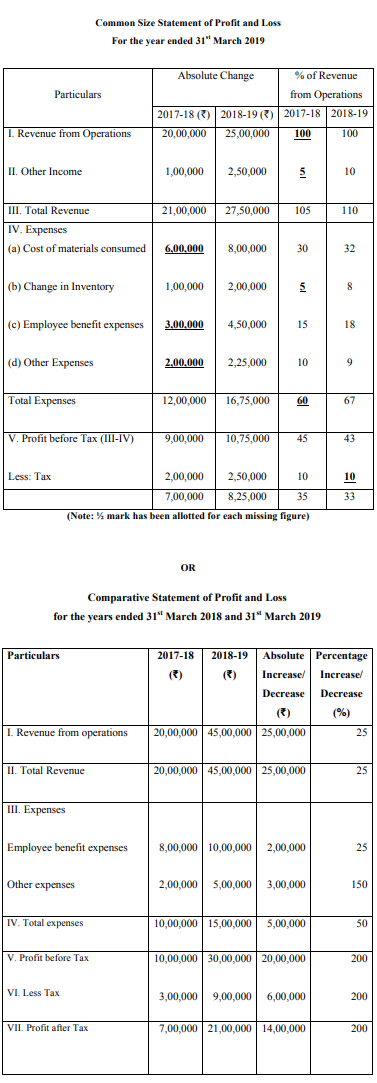

Question 31: (Marks 4)

Fill in the amounts left blank in the following Common Size Statement of Profit and Loss for the year ended 31st March, 2019.

Answer :

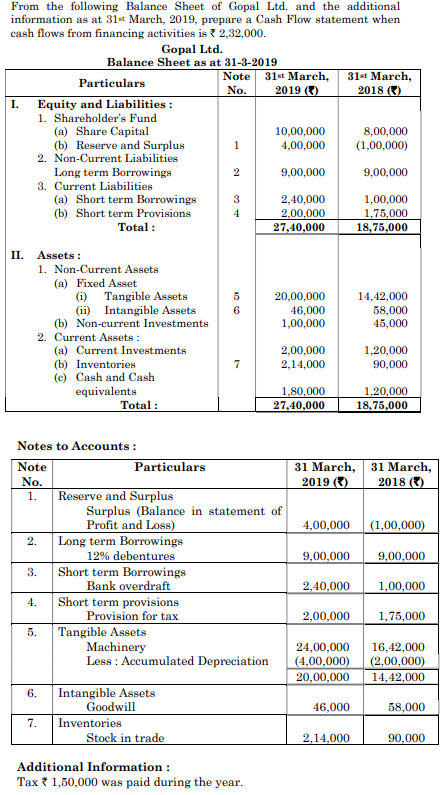

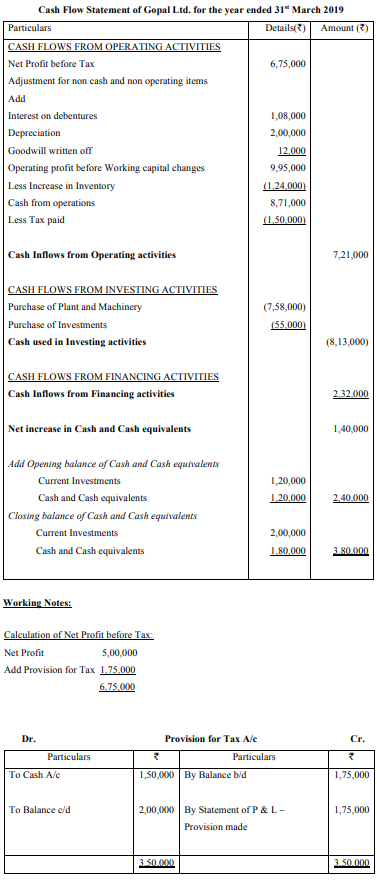

Question 32: (Marks 4)

Answer :

(Computerized Accounting)

Question 23: (Marks 1)

The process of comparing input data with some known data is called

(a) storage data

(b) information data

(c) data validation

(d) data entry

Answer :

(c) / Data validation

Question 24: (Marks 1)

A ______ attribute can be divided into smaller sub-parts but a _____ attribute cannot be further sub divided.

Answer :

A composite attribute can be divided into smaller sub-parts but a simple attribute cannot be further sub divided.

Question 25: (Marks 1)

Name the accounting information sub-system which deals with receipt and payment of physical cash and electronic fund transfer.

(a) Cash and Bank sub-system.

(b) Sales and accounts receivable sub-system.

(c) Purchase and accounts payable sub-system.

(d) Costing sub-system.

Answer :

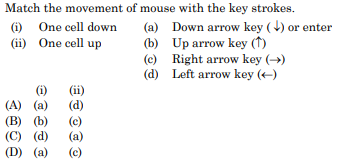

(a) / Cash and Bank sub-system

Question 26: (Marks 1)

Answer :

(a) Down arrow key (ê)

Question 27: (Marks 1)

_______ prompts the user to enter parameters or criteria through an input box for selecting a set of records with different criteria.

Answer :

Parameter query

Question 28: (Marks 1)

Hardware refers to

(a) System software and application software.

(b) Computer associated peripherals and their network.

(c) A logical sequence of actions to perform a task.

(d) All of the above.

Answer :

(b)/ Computer associated peripherals and their network

Question 29: (Marks 1)

Rows are referred by alpha characters and columns are numerically numbered from top to bottom. (True/False)

Answer :

False.

Question 30: (Marks 3)

State any three features of good Accounting Software.

OR

Name the function of Excel which converts numeric value to text in a specific number format. Explain its syntax.

Answer :

Following are the features of good accounting software (Any three):

(a) Do all basic accounting functions

(b) Manage your stored data and stores

(c) Do the job for costing

(d) Manage payroll

(e) Get many MIS (Management information system)

(f) File tax return (g) Maintain budget etc

(h) Calculate interest pending amounts

(i) Manage data over different locations and synchronize it and many more other features.

OR

The name of the function is ‘TEXT’

Its syntax is

TEXT ( value, format _ text)

Value - numeric value which, evaluates a numeric value or referenced cell containing numeric value.

Formal Text – is a numeric format as a text string enclosed in quotation mark.

Question 31: (Marks 4)

Why is it necessary to have safety features in accounting softwares ? Explain any two tools which provide data security.

OR

What is meant by # DIV/O ! Error ? State the reasons for the error.

Answer :

It is necessary to have safety features in accounting software to maintain the secrecy of accounting data.

Tools which provide data security: (Any two)

1) Password Security : Password is widely accepted security control to access the data. Only the authorized person can access the date. Any user who does not know the password cannot retrieve information from the system. It ensures data integrity. It was a binary according format of storage and offers access to the data base.

2) Data audit : Audit feature of accounting software provides the user with administrator right in order to keep track of unauthorized access to the database. It audits for the correctness of entries. Once entries are audited with adulteration, if any, the software displays all along with the name of the auditor user and date and – lime of attention.

3) Data Vault : Software provides additional security for the imputed data and this feature is referred as data vault. Data vault ensures that original information is presented and is not tempered. Data vault password cannot be broken. Some software’s even use data encryption method.

OR

This means an error where the number is divided by zero (0).

Reasons

(i) Entering a formula that contains explicit division by zero (0) e.g. = 5/0

(ii) Using the cell reference to a blank cell or to a cell that contains zero as a division to correct this. Either your need to change the cell reference or put a value in the cell used as a divisor

Question 32: (Marks 6)

‘A Ltd.’ wants to enter their sales related data on excel sheet, for their three products to prepare a graphic presentation to be presented in the Board Of Directors meeting.

State the basic steps to prepare presentation.

Answer :

The basic steps to prepare a presentation to present sales related data are:

1) Collect data from various departments, heads/division for each quarter.

2) The data to be entered on excel sheet for different quarters before the product in consideration.

3) Total sale for all the product and single product for all different quarters be calculated by summing up rows and columns.

4) Select to plot product wise total sales. Into a chart by selecting chart type (use insert tab and click on chart.)

5) To draw a chart/graph for the given data, the data worksheet should be reorganised.

6) Draw a chart or variety of chart mixing up the options to be presented in the meeting.

Accountancy sample paper class 12, Accountancy previous year question paper class 12, cbse class 12 Accountancy sample paper, cbse class 12 Accountancy sample paper 2020, Accountancy sample paper class 12 2020, cbse sample paper 2020 class 12 Accountancy, class 12 Accountancy sample paper 2020, class 12 important questions Accountancy, cbse class 12 board exam Accountancy paper, Accountancy previous year question papers class 12 with solutions, Accountancy sample paper class 12 2019, cbse class 12 Accountancy question paper 2017 solved pdf, cbse class 12 Accountancy question paper 2018, class 12 Accountancy paper 2019, Accountancy question paper for class 12, cbse class 12 Accountancy paper 2019

Copyright @ ncerthelp.com A free educational website for CBSE, ICSE and UP board.