Here we are providing CBSE Previous Year Question Papers Class 6 to 12 solved with soutions CBSE Class 12th Accountancy Question Paper Solved Last 10 Years with Solution Accountancy sample paper class 12, Accountancy previous year question paper class 12, cbse class 12 Accountancy sample paper, cbse class 12 Accountancy sample paper 2020, Accountancy sample paper class 12 2020, cbse sample paper 2020 class 12 Account Practice of previous year question papers and sample papers protects each and every student to score bad marks in exams.If any student of CBSE Board continuously practices last year question paper student will easily score high marks in tests. Fortunately earlier year question papers can assist the understudies with scoring great in the tests. Unraveling previous year question paper class 12 Accountancy is significant for understudies who will show up for Class 12 Board tests.

PART – A

(Accounting for Not-For-Profit-Organisations, Partnership Firms and Companies)

Question 1: (Marks 1)

Disha and Abha were partners in a firm. Farad was admitted as a new partner for 1/5th share in the profits of the firm. Farad brought proportionate capital. Capitals of Disha and Abha after all adjustments were ₹ 64,000 and ₹ 46,000 respectively. Capital brought by Farad was :

(a) ₹ 22,000

(b) ₹ 27,500

(c) ₹ 55,000

(d) ₹ 28,000

Answer :

(b)/ ₹27,500

Question 2: (Marks 1)

Which of the following is not a capital receipt ?

(a) Donations for tournament

(b) Donations for building fund

(c) Life membership fee

(d) Entrance fees

Answer :

(d)/ Entrance Fees

Question 3: (Marks 1)

What is meant by ‘Authorised Capital’ ?

Answer :

Authorised Capital is the maximum amount of capital which a company is authorized to have.

Or

Authorised Capital is the maximum amount of capital which a company can issue in its entire lifetime.

Question 4: (Marks 1)

Saurabh, Shirin and Somesh are partners in a firm sharing profits and losses in the ratio of 3:2:1. Somesh retires and the new profit sharing ratio between Saurabh and Shirin is 3:2. The gaining ratio between Saurabh and Shirin will be :

(a) 3:2

(b) 3:1

(c) 1:1

(d) 2:1

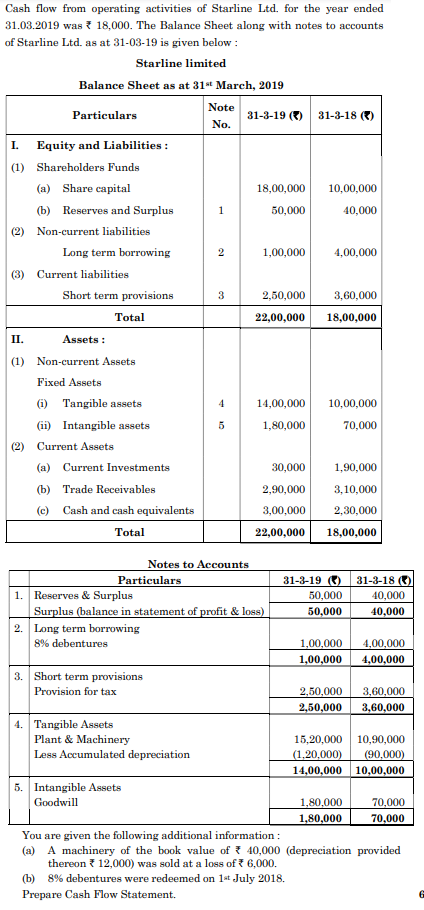

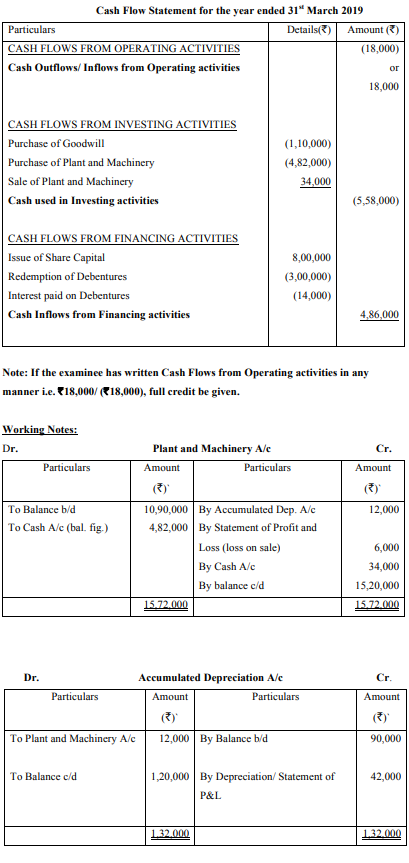

Answer :

(a)/ 3:2

Question 5: (Marks 1)

Mohit and Rohit were partners in a firm with capitals of ₹ 80,000 and ₹ 40,000 respectively. The firm earned a profit of ₹ 30,000 during the year. Mohit’s share in the profit will be :

(a) ₹ 20,000

(b) ₹ 10,000

(c) ₹ 15,000

(d) ₹ 18,000

Answer :

(c)/ ₹15,000

Question 6: (Marks 1)

In case of retirement of a partner, profit or loss on revaluation of assets and re-assessment of liabilities is distributed among _______ partners in _______ ratio.

Answer :

In case of retirement of a partner, profit or loss on revaluation of assets and reassessment of liabilities is distributed among the old partners in the old ratio.

Question 7: (Marks 1)

Vanya Ltd. forfeited 20,000 equity shares of ` 100 each for non-payment of first and final call of ₹ 40 per share. The maximum amount of discount at which these shares can be re-issued will be :

(a) ₹ 8,00,000

(b) ₹ 12,00,000

(c) ₹ 20,00,000

(d) ₹ 20,000

Answer :

(b)/ ₹12,00,000

Question 8: (Marks 1)

_________ means any offer of securities to a select group of persons by a company other than by way of public offer.

Answer :

Private Placement means any offer of securities to a select group of persons by a company other than by way of public offer.

Question 9: (Marks 1)

Shahi Ltd. decided to redeem its 8,000, 11% debentures of ₹ 100 each at a premium of 10%. The minimum amount transferred to debenture redemption reserve will be :

(a) ₹ 8,00,000

(b) ₹ 4,00,000

(c) ₹ 2,00,000

(d) ₹ 2,20,000

Answer :

(c)/ ₹2,00,000

Question 10: (Marks 1)

Which of the following does not result into reconstitution of a firm ?

(a) Dissolution of partnership firm.

(b) Dissolution of partnership.

(c) Change in profit-sharing-ratio of existing partners.

(d) Death of partner.

Answer :

(a)/ Dissolution of partnership firm.

Question 11: (Marks 1)

Jaipur Club has a prize fund of ` 6,00,000. It incurs expenses on prizes amounting to ` 5,20,000. The expenses should be

(a) debited to income and expenditure account.

(b) presented on the asset side of the balance sheet.

(c) debited to income and expenditure account and presented on the asset side of the balance sheet.

(d) deducted from the prize fund on the liability side of the balance sheet.

Answer :

(d)/ deducted from the Prize Fund on the liability side of the balance sheet

Question 12: (Marks 1)

No debenture redemption reserve is required for debentures issued by :

(a) manufacturing companies

(b) infrastructure companies

(c) banking companies

(d) trading companies

Answer :

(c)/ Banking companies

Question 13: (Marks 1)

The portion of uncalled capital to be called only in the event of winding up of the company is called _________.

Answer :

Reserve Capital

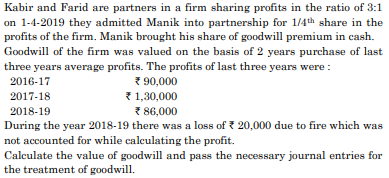

Question 14: (Marks 3)

OR

Raka, Seema and Mahesh were partners sharing profits and losses in the ratio of 5:3:2. With effect from 1st April, 2019, they mutually agreed to share profits and losses in the ratio of 2:2:1. On that date, there was a workmen’s compensation fund of ₹ 90,000 in the books of the firm. It was agreed that :

(i) Goodwill of the firm be valued at ₹ 70,000.

(ii) Claim for workmen’s compensation amounted to ₹ 40,000.

(iii) Profit on revaluation of assets and re-assessment of liabilities amounted to ₹ 40,000.

Pass necessary journal entries for the above transactions in the books of the firm.

Answer :

Calculation of goodwill

Average Profits = (₹90,000 + ₹1,30,000 + ₹86,000)/3

=₹1,02,000

Goodwill = ₹1,02,000 x 2

= ₹2,04,000

Question 15: (Marks 4)

Answer :

Question 16: (Marks 4)

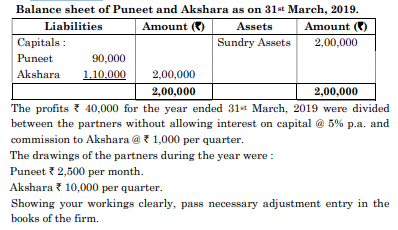

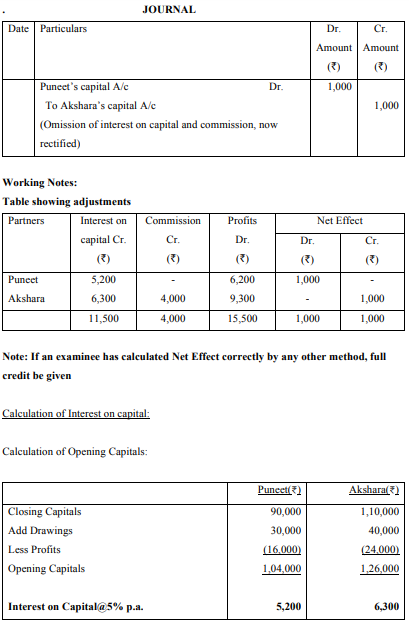

Puneet and Akshara were partners in a firm sharing profits and losses in the ratio of 2:3. The following was the balance sheet of the firm as on 31st March, 2019.

Answer :

Question 17: (Marks 4)

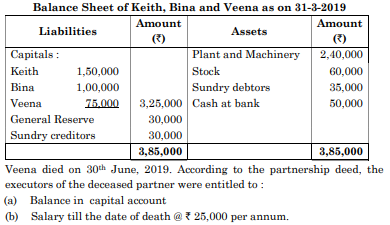

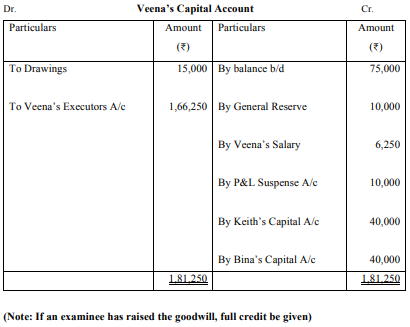

Keith, Bina and Veena were partners in a firm sharing profits and losses equally. Their balance sheet as on 31-3-2019 was as follows :

(c) Share of goodwill calculated on the basis of twice the average profits of past three years.

(d) Share of profit from the closure of the last accounting year till the date of death on the basis of average of three completed years profits before death.

(e) Profits for 2016-17, 2017-18 and 2018-19 were ₹ 1,20,000, ₹ 90,000 and ₹ 1,50,000 respectively. Veena withdrew ₹ 15,000 on 1st June, 2019 for paying her daughter’s school fees.

Prepare Veena’s capital account to be rendered to her executors.

Answer :

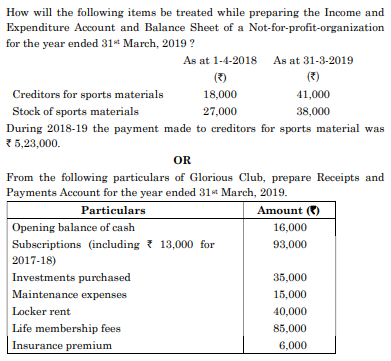

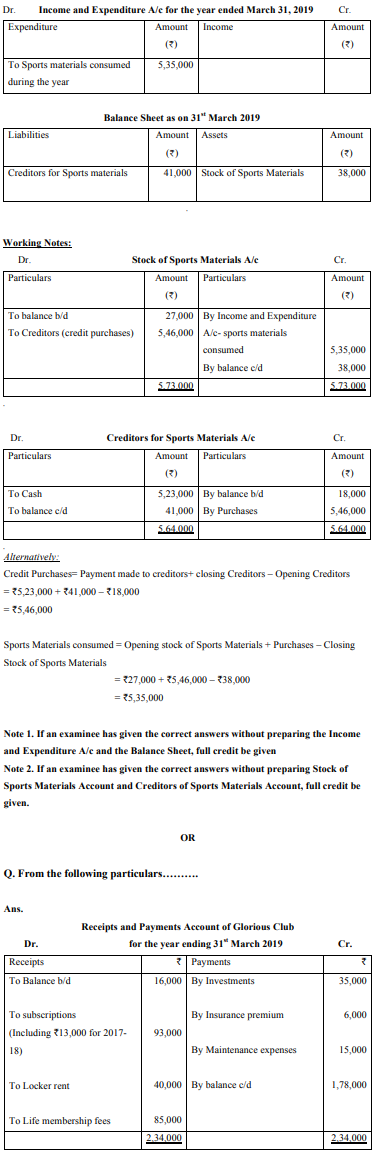

Question 18: (Marks 4)

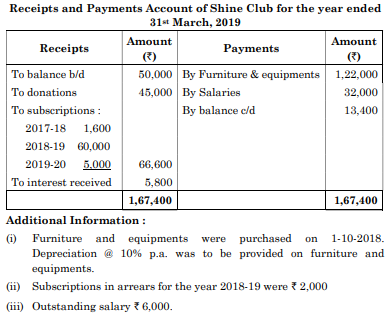

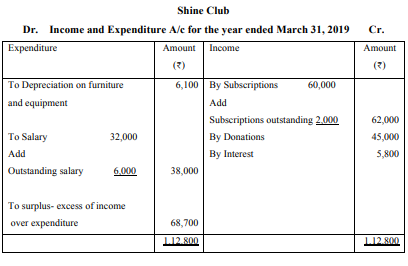

From the given Receipts and Payments Account and additional information of Shine Club for the year ended 31st March, 2019, prepare Income and Expenditure Account for the year ended 31st March, 2019.

Answer :

Question 19: (Marks 6)

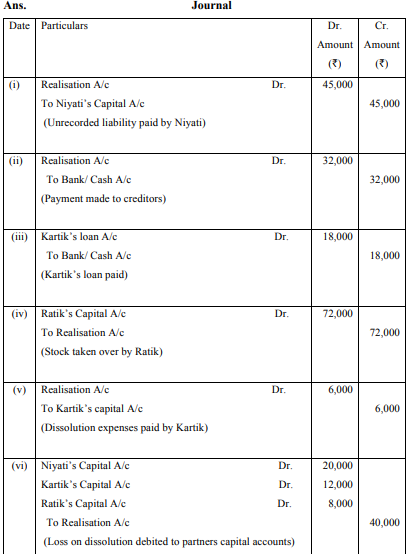

Niyati, Kartik and Ratik were partners in a firm sharing profits and losses in the ratio of 5:3:2. The firm was dissolved on 31st March, 2019 by the order of the court. After transfer of assets (other than cash) and external liabilities to Realization Account, the following transactions took place :

(a) An unrecorded liability of the firm of ₹ 45,000 was paid by Niyati.

(b) Creditors, to whom ₹ 67,000 were due to be paid, accepted furniture at ₹ 35,000 and the balance was paid to them in cash.

(c) Kartik had given a loan of ₹ 18,000 to the firm which was paid to him.

(d) Stock worth ₹ 85,000 was taken over by Ratik at ₹ 72,000.

(e) Expenses on dissolution amounted to ₹ 6,000 and were paid by Kartik.

(f) Loss on dissolution amounted to ₹ 40,000. Pass the necessary journal entries for the above transactions in the books of the firm.

Answer :

Quwestion 20: (Marks 6)

(a) On 1st April, 2015, Mayfair Ltd. issued 4,000 9% debentures of ₹ 100 each at a discount of 5% redeemable at a premium of 8%. The debentures were redeemable on 31st March, 2019. The company created the necessary minimum amount of debenture redemption reserve and purchased the required amount of debenture redemption investments as per the provisions of Companies Act, 2013.

Pass the necessary journal entries for redemption of debentures.

(b) Hero Ltd. purchased plant and machinery for ₹ 18,00,000 from Pearl Machines Ltd. payable ₹ 3,00,000 by drawing a promissory note and the balance by issue of 9% debentures of ₹ 100 each at a premium of 20%.

Pass the necessary journal entries in the books of Hero Ltd. for the above transactions.

OR

(a) BGP Ltd. invited applications for issuing 15,000, 11% debentures of ₹ 100 each at a premium of ` 50 per debenture. The full amount was payable on application. Applications were received for 25,000 debentures. Applications for 5,000 debentures were rejected and the application money was refunded. Debentures were allotted to the remaining applicants on pro-rata basis.

Pass the necessary journal entries for the above transactions in the books of BGP Ltd.

(b) Agam Ltd. issued 40,000 9% debentures of ₹ 100 each on April 1, 2018 at a discount of 10%, redeemable at a premium of 10%. Assuming that the interest was paid half yearly on September 30 and March 31 and the tax deducted at source was 10%, give journal entries relating to debenture interest for the half year ended March 31, 2019.

Answer :

Question 21: (Marks 8)

Premier Tools Ltd. invited applications for issuing 2,00,000 equity shares of ₹ 10 each at a premium of ₹ 2 per share. The amount was payable as follows :

On application - ₹ 5 per share (including premium)

On allotment - ₹ 3 per share

On first & final call – Balance

Applications were received for 2,50,000 shares. Applications for 10,000 shares were rejected and pro-rata allotment was made to the remaining applicants. Over payments received on application were adjusted towards sums due on allotment.

All calls were made and duly received except allotment and first and final call from Naveen who applied for 7,200 shares. His shares were forfeited. Half of the forfeited shares were reissued for ₹ 48,000 as fully paid. Pass the necessary journal entries for the above transactions in the books of Premier Tools Ltd. Open calls-in-arrears account wherever required.

OR

Concept Stationary Ltd. invited applications for issuing 3,00,000 shares of ₹ 10 each at a premium of ₹ 3 per share. The amounts were payable as follows :

On application and allotment – ₹ 7 per share.

On first & final call – balance (including premium of ₹ 3)

Applications were received for 4,00,000 shares & allotment was made as follows :

(i) To applicants for 80,000 shares – 80,000 shares.

(ii) To applicants for 40,000 shares – nil

(iii) Balance of the applicants were allotted shares on pro-rata basis.

Excess money received with applications was adjusted towards sums due on first and final call.

Amit, who belonged to category (i) and was allotted 4,000 shares and Veni, who belonged to category (iii) and was allotted 4,400 shares failed to pay the first and final call money. Their shares were forfeited. The forfeited shares were re-issued at ₹ 7 per share fully paid-up.

Pass necessary journal entries for the above transactions in the books of the company.

Answer :

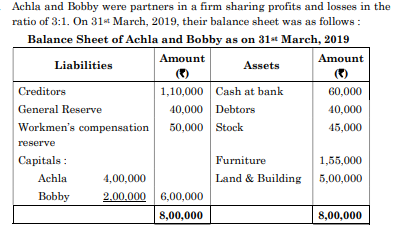

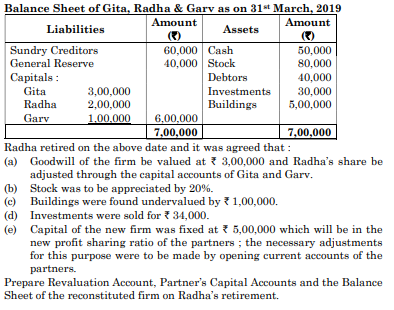

Question 22: (Marks 8)

On 1st April, 2019, they admitted Vihaan as a new partner for 1/5th share in the profits of the firm on the following terms :

(a) Vihaan brought ₹ 1,00,000 as his capital and the capitals of Achla and Bobby were to be adjusted on the basis of Vihaan’s capital ; any surplus or deficiency was to be adjusted by opening current accounts.

(b) Goodwill of the firm was valued at ₹ 4,00,000. Vihaan brought the necessary amount in cash for his share of goodwill premium, half of which was withdrawn by the old partners.

(c) Liability on account of workmen’s compensation amounted to ₹ 80,000.

(d) Achla took over stock at ₹ 35,000.

(e) Land and building was to be appreciated by 20%.

Prepare Revaluation Account, Partner’s Capital Accounts and the Balance Sheet of the reconstituted firm on Vihaan’s admission.

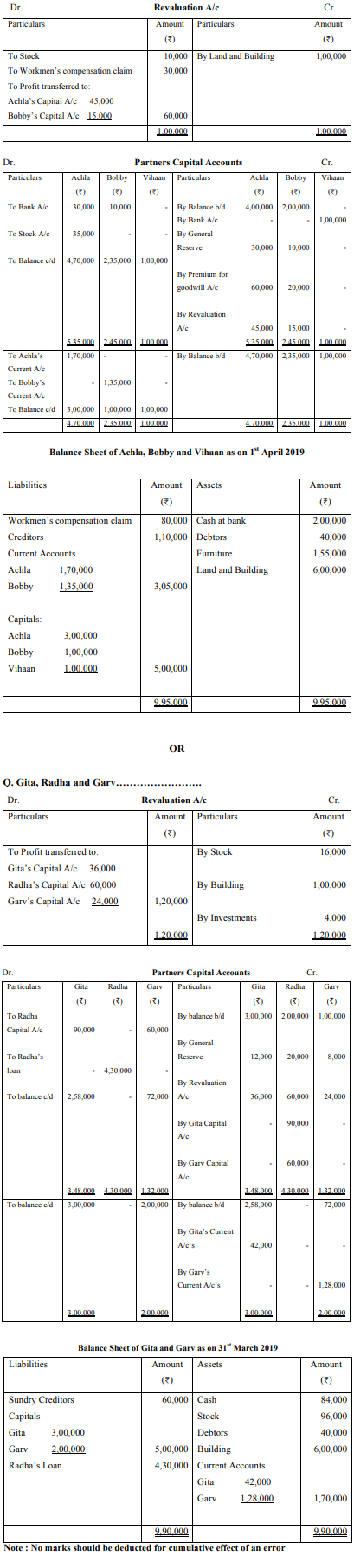

OR

Gita, Radha and Garv were partners in a firm sharing profits and losses in the ratio of 3:5:2. On 31st March, 2019, their balance sheet was as follows :

Answer :

Option – I

(Analysis of Financial Statements)

Question 23: (Marks 1)

State the primary objective of preparing cash flow statement.

Answer :

The objective of Cash Flow Statement is to provide useful information about Cash Flows (Inflows & outflow) of an enterprise during a particular period under various heads of activities

Question 24: (Marks 1)

From the following information, calculate the amount of cash flow from investing activities. Acquired machinery for ₹ 10,00,000, paying 10% immediately in cash and accepting a draft for the balance in favour of the vendor, payable after three months.

Answer :

Cash outflow from investing activity (₹1,00,000)

Question 25: (Marks 1)

State giving reason, whether issue of shares for consideration other than cash will result into inflow, outflow or no flow of cash.

Answer :

No flow of cash

Reason: There is no change in cash and cash equivalents

Question 26: (Marks 1)

Which of the following is not a tool of financial analysis ?

(a) Comparative income statement

(b) Comparative position statement

(c) Statement of profit and loss

(d) Cash flow statement

Answer :

(c)/ Statement of profit and loss

Question 27: (Marks 1)

Which of the following is a limitation of financial analysis ?

(a) It is just a study of reports of the company.

(b) It judges the ability of the firm to repay its debts.

(c) It identifies the reasons for change in financial position.

(d) It ascertains the relative importance of different components of the financial position of the firm.

Answer :

(a)/ It is just a study of reports of the company

Question 28: (Marks 1)

As per Schedule III, Part I of the Companies Act, 2013 ‘calls-in-arrears’ will be presented under which of the following head/sub-head, in the Balance Sheet of a company ?

(a) Reserves and Surplus

(b) Current Liabilities

(c) Contingent Liabilities

(d) Shareholders Funds

Answer :

(d)/ Shareholders Funds

Question 29: (Marks 1)

‘Interest accrued but not due on loans’ is shown in the companies balance sheet under the sub head _________.

Answer :

Other Current Liabilities

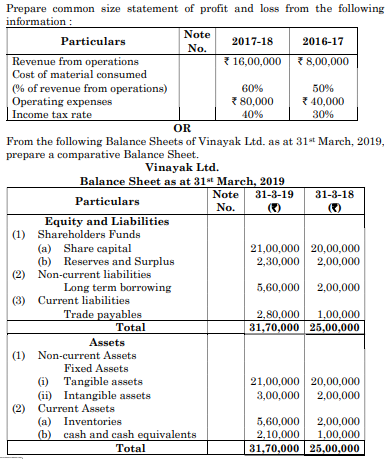

Question 30: (Marks 3)

A company had a liquid ratio of 1.5:1 and a current ratio of 2:1. Its inventory turnover ratio was 6 times. It had total current assets of ₹ 2,00,000. Find out revenue from operations if the goods are sold at 25% profit on cost.

OR

Calculate the amount of opening trade receivables and closing trade receivables from the following information :

Trade receivables turnover ratio 8 times

Cost of revenue from operations ₹ 4,80,000

The amount of credit revenue from operations is ₹ 2,00,000 more than cash revenue from operations. Gross profit ratio is 20%. Opening trade receivables are 1/4th of Closing trade receivables.

Answer :

Current Ratio = Current Assets/ Current Liabilities

ð 2 = ₹2,00,000/ Current Liabilities

ð Current Liabilities = ₹1,00,000

Quick Ratio = Quick Assets/ Current Liabilities……………………………..…..1/2

ð 1.5 = Quick Assets/ ₹1,00,000

ð Quick Assets = ₹1,50,000…………………………………………..…....1/2

Average Inventory= Current Assets – Quick assets

=₹2,00,000 – ₹1,50,000

=₹50,000

Inventory Turnover Ratio = Cost of Revenue from operations/ Average Inventory… 1/2

ð 6 = Cost of Revenue from operations/ ₹50,000

ð Cost of Revenue from operations = ₹3,00,000…………………………….…1/2

Gross profit = ¼ x ₹3,00,000

= ₹75,000

Revenue from operations = Cost of Revenue from operations + Gross profit

= ₹3,00,000 + ₹75,000

= ₹3,75,000 ……………………………..…………………1

(If an examinee has arrived at the correct answer using alternative method, full credit be given)

OR

Trade Receivables Turnover Ratio = Credit Revenue from operations/ Average Trade

Receivables………………………………………………………………………....1/2

Cost of Revenue from operations = 4,80,000

Gross profit = ¼ x ₹4,80,000

= ₹1,20,000

Revenue from operations= Cost of Revenue from operations + Gross profit

= ₹4,80,000 + ₹1,20,000

= ₹6,00,000……………………………………&hhellip;…………....1/2

Revenue from operations = Cash Revenue from operations + Credit Revenue from operations

ð ₹6,00,000 = Cash Revenue from operations + (₹2,00,000 + Cash Revenue from operations)

ð Cash Revenue from operations= ₹2,00,000

ð Credit Revenue from operations=

₹4,00,000……………………..………………....1

Trade Receivables Turnover Ratio = Credit Revenue from operations/ Average Trade Receivables

ð 8 = ₹4,00,000/ Average Trade Receivables

ð Average Trade Receivables = ₹50,000

ð (Opening Trade Receivables + closing Trade Receivables)/2 =₹50,000

ð (¼ closing Trade Receivables + closing Trade Receivables)/2 =₹50,000

ð Closing Trade Receivables

= ₹80,000…………………….……………………....1/2

ð Opening Trade Receivables

= ₹20,000…………………………………………....1/2

(If an examinee has arrived at the correct answer using alternative method, full credit be given)

Question 31: (Marks 4)

Answer :

Question 32: (Marks 6)

Answer :

Option – II

(Computerized Accounting)

Question 23: (Marks 1)

_________ is a logical action to perform a task.

(a) Data

(b) Hardware

(c) System

(d) Procedure

Answer :

(d) Procedure

Question 24: (Marks 1)

Name of account, (i) _________, (ii) _________ and amount are the four forms of data elements of a transaction in computerized accounting.

Answer :

Name of account, (i) Accounting code, (ii) Date of transaction and amount are the four forms of data elements of a transaction in computerized accounting.

Question 25: (Marks 1)

Cell address refers to

(a) location of cell

(b) group of cells

(c) cell reference

(d) All of these

Answer :

(d) / All of above

Question 26: (Marks 1)

To expect a well formatted printable data from access database, we use

(a) Table

(b) Form

(c) Report

(d) Query

Answer :

(c) / Report

Question 27: (Marks 1)

A spreadsheet is used (i) _________ calculate and compare (ii) _________ or financial data.

Answer :

A spreadsheet is used (i) record, calculate and compare (ii) numerical or financial data.

Question 28: (Marks 1)

A sequential code helps either (i) in _________ or (ii) _________ a relevant document.

Answer :

A sequential code helps either (i) in Identification of missing codes or (ii) Trace a relevant document.

Question 29: (Marks 1)

The interactive link between the user and data base oriented software through which the user communicates is known as

(a) Front end interface

(b) Back end interface

(c) Data processing

(d) Reporting system

Answer :

(a) / Front end interface

Question 30: (Marks 3)

State any three requirements which should be considered before making an investment to choose between ‘Desktop Database’ or ‘Server Database’.

OR

Explain any three types of vouchers used for facilitating entry in ‘Tally Software’.

Answer :

The points to be considered before making investment in a database are (any three)

(i) What all data to be stored in database

(ii) Who will capture or modify the data and how frequently the data will be modified.

(iii) Who will be using database to perform what type of tasks.

(iv) Will the database (backend) be used by any other frontend application.

(v) Will access to database be given over LAN/internet and for what purpose?

(vii) What level of hardware and operating system is available?

OR

Types of vouchers (Any three)

(i) Contra voucher: Used for fund transfer between cash and Bank A/c only. If cash is withdrawn from Bank for office or deposited in the Bank from office this voucher will be used.

(ii) Receipt Voucher: All the inflow of money is recorded through receipt voucher. Such receipts may be toward any income such as receipts from Debtors, loan/advance taken or refund of loan/advance etc.

(iii) Payment Voucher: All outflow of money is recorded through payment voucher such payments may be towards any purchases, Expenses, due to creditors, loan/advance etc.

(iv) Journal Voucher: It is an adjustment voucher, normally used for non-cash transactions like adjustment between ledgers.

Question 31: (Marks 4)

Write and explain the formulae to calculate basic pay earned and total earnings.

OR

What is meant by a ‘Form’ ? How is ‘split form’ different from ‘simple form’ ?

Answer :

Basic Pay Earned is calculated with reference to number of effective days present.

BPE = BP x NOEDP/ NOPM

Where NOEDP is Number of effective days present.

NODM = Number of days in a month total earning will include.

DA = BPE x applicable rate

HRA = BPE x applicable rate

Transport allowance : Either fixed or applicable rate

Total Earnings = TE

TE = BPE + DA + HRA + TRA

OR

Form: Access provides a user friendly interface which allows user to enter information in a graphical way. It is known as Form. This information transparently passed to the underlying database.

Split Form : This presentation shows underlying database in one half of the section and form in other half for entering information in the record selected in the data sheet. The two views in the form one synchronized so that scrolling in one view causes scrolling of other half to facilitate view of the same location of the record.

Question 32: (Marks 6)

Star Ltd. has a sales linked bonus policy to motivate its sales personnel. Any employee achieving target sales for the month is paid ₹ 5,000 as bonus. There is an additional incentive of 2% of the amount of sales exceeding the target sales (i.e., the difference in target sales and actual sales). The target sale for current month was 1500 units.

Calculate the bonus for employees mentioned below and also give the excel formula for the same.

(a) Amit sold 700 units for ₹ 7,00,000

(b) Namit sold 1500 units for ₹ 15,00,000

(c) Jatin sold 2,200 units for ₹ 22,00,000

Answer :

Keys A1 = Employee Name

B1 = Achieved Sales

C1 = Target Sales

D1 = Difference (C1-B1)

E1 = Bonus

(a) E1 = If (D1 = 0,5000, If (D1 >0, 5000 + 0.02D1,0))

Amit = 0

(b) E2 = If (D2 = 0,5000, If (D2 >0, 5000 + 0.02D2,0))

Namit = ₹5000

(c ) If (D3 = 0,5000, If (D3>0, 5000 + 0.02D3,0))

Jatin = ₹19,000

Note: If an examinee has written just the amounts and no formulae, only ½ mark per calculation be given.

Accountancy sample paper class 12, Accountancy previous year question paper class 12, cbse class 12 Accountancy sample paper, cbse class 12 Accountancy sample paper 2020, Accountancy sample paper class 12 2020, cbse sample paper 2020 class 12 Accountancy, class 12 Accountancy sample paper 2020, class 12 important questions Accountancy, cbse class 12 board exam Accountancy paper, Accountancy previous year question papers class 12 with solutions, Accountancy sample paper class 12 2019, cbse class 12 Accountancy question paper 2017 solved pdf, cbse class 12 Accountancy question paper 2018, class 12 Accountancy paper 2019, Accountancy question paper for class 12, cbse class 12 Accountancy paper 2019

Copyright @ ncerthelp.com A free educational website for CBSE, ICSE and UP board.